Key findings from the PeakSpan Ibbaka Net Revenue Retention Research

The PeakSpan Ibbaka Net Revenue Retention Survey Results for 2024 are now available. This is the second year we have done this survey together. This year’s survey gathers the responses from more than 500 B2B SaaS companies.

You can request a copy of the report here.

Here are the key findings from the survey.

Key findings

- There is a growing cluster of disruptive companies with emergent patterns for NRR performance

- Some of the companies in this cluster have the unexpected pattern of high churn with high revenue expansion leading to high NRR

- Dedicated teams responsible for expansion revenue are outperforming other organizational designs

- There are some early indications that M2M (Machine to Machine) companies will have strong NRR performance once they get traction

- Packaging patterns have an impact on NRR performance - design packaging to enable cross-selling and upselling

Growing cluster of disruptive companies

We used the Leiden algorithm to cluster the survey responses and found three distinct clusters. The Conventional and Enterprise clusters could have been found in last year’s survey results. It is the Emerging cluster that is driving change. The Emerging cluster was by far the largest cluster.

We believe this cluster reflects the disruption being caused by generative AI. All companies in the General AI vertical and most of the companies using pricing metrics associated with generative AI (tokens, models, agent-based) are in this cluster.

The companies with the best NRR performance were in this cluster, but the distribution of NRR performance was bimodal: there was a group of high-performing companies and a group of lower performers.

The unexpected pattern of high churn with high revenue expansion

This was the most surprising result. One generally assumes that a company with high churn will have a low NRR. And that when churn is high the priority must be to get churn under control. This year’s results lead us to question that assumption. There were a number of companies that combined high churn with high NRR, driven by very high expansion revenue. What is happening?

Above is one example. Most of us would be alarmed to have a churn of 20% but would do just about anything to have expansion revenue of 110%.

We hypothesize that some companies, primarily in AI and adjacent areas, are casting a wide net to find customers who get exceptional value and that they can grow quickly. They are OK to let other customers, who get less value, churn. We expect this is a short-term phenomena that reflects the rapid growth and changing use cases for generative AI applications. But what if we are wrong? It could be that there is a compelling business strategy that is based on casting a wide net and only keeping the companies that will drive exceptional growth.

The full report includes additional examples of NRR, churn, and expansion revenue for specific companies.

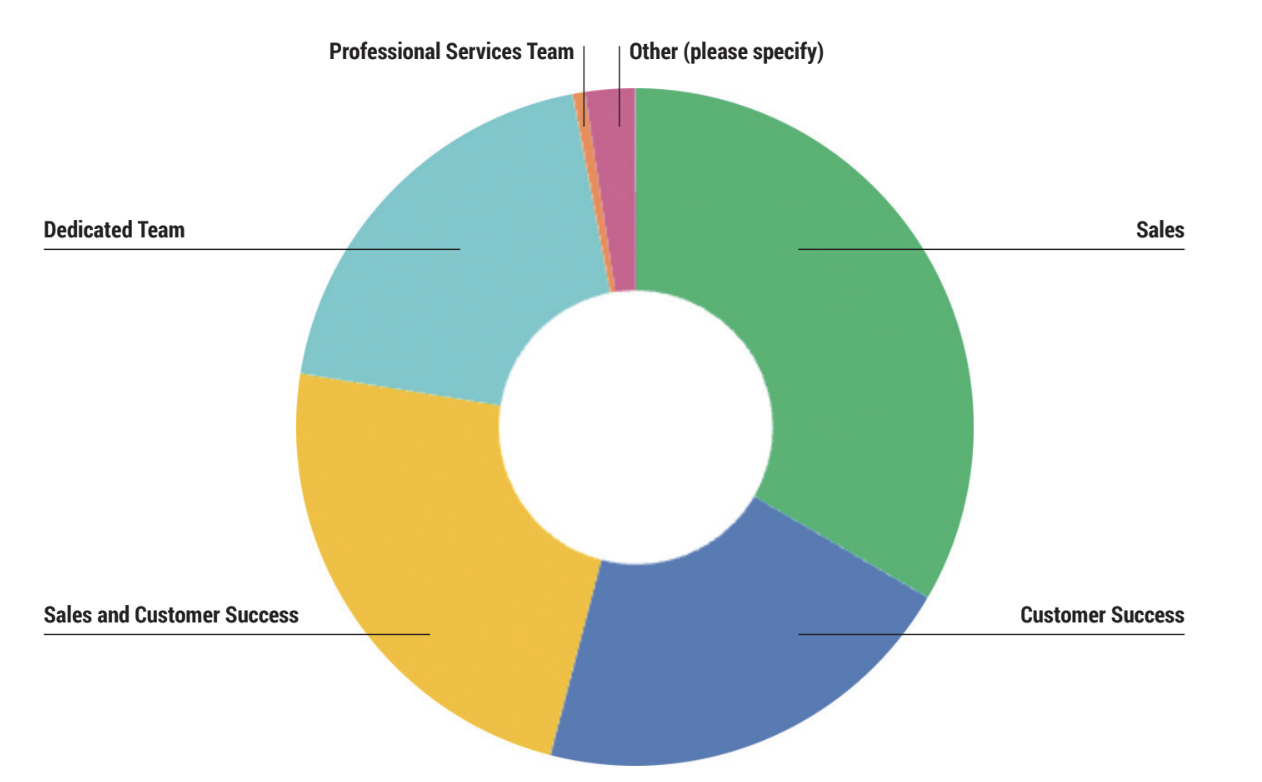

Dedicated teams responsible for expansion revenue are outperforming

Companies have tried many different organizational approaches to renewals. Some rely on their sales teams, others have customer success take the lead, and there are others that use a combined team. In 2024 though, it was companies with teams dedicated to expansion revenue that dominated the top of the table.

It seems that the key here is to focus on expansion revenue ahead of renewal. If a customer is growing their use and the value they are receiving they will in any case be unlikely to churn.

Early indications that M2M companies will have strong NRR performance

Most focus in SaaS is one B2B and B2G, with B2C, social media, and consumer eCommerce being treated somewhat separately. There is another way to think about this though, M2M or Machine to Machine business models. In this year’s survey, there were only a smattering of companies focused on M2M business models, mostly from the Data Feed Management or API Integrator spaces. The Data Feed Management space seems to be getting a big boost from AIOps or MLOps (both terms are used).

These companies are delivering very good NRR performance. We have to be careful here, as the N is only 23 (4.6% of the total), but companies in M2M had an enviable average NRR of 131%, average churn was relatively high at 7% and average expansion revenue was strong at 24%.

These solutions tend to be deeply integrated with other systems (relatively low churn in a dynamic market) and priced to scale with use (strong expansion revenue).

Packaging patterns have an impact on NRR performance

One important result is that the packaging pattern has an impact on NRR. Ibbaka has identified ten packaging patterns common in B2B SaaS (these will be revised in 2025 to reflect emerging patterns from generative AI).

The highest expansion revenues were for API Integrators and Data Feed Managers, where a lot of the growth is being driven by MLOps and AIOps. On the other hand, the One Big Package (often seen at early-stage companies) and Tired (GBB) patterns underperformed.

Surprisingly (to me anyway), API Integrators had high churn. This is counterintuitive as this pattern is thought to be quite sticky. Once you have integrated an API it is often easiest to leave things be. Perhaps the experimentation associated with the adoption of generative AI is destabilizing this.

There are many other insights available in the report, and this year we have share more of the data should you want to dig in yourself.

Sanket has worked with growth-stage software businesses throughout his career and has served on more than 12 boards. Today, he is one of four Partners on the team and leads the firm's coverage of both Cyber & Digital Infrastructure and EdTech. Sanket joined PeakSpan just one year after its founding in 2016 as one of the first non-founding team members and has helped build the firm from two investments and $150M in Fund I to more than $2.5B in AUM, backing applied AI and B2B software companies on the journey from $3–10M to beyond $50M in ARR.

Before joining PeakSpan, Sanket worked in the Technology, Media & Telecom Group at Houlihan Lokey, focusing exclusively on software M&A and private financing transactions for $10–50M ARR companies through critical inflection points such as selling, raising capital, or recapitalizing. Before Houlihan Lokey, Sanket was a Global Banking and Brokerage Group Consultant at FactSet Research Systems, where he partnered with investment banking, private equity, and venture capital clients.

Sanket holds a B.B.A. in Finance with a minor in Economics from the Leeds School of Business at the University of Colorado at Boulder. Sanket jokes that he's grown up at PeakSpan, having celebrated some remarkable personal milestones while with the firm, including getting engaged and married to his wife, Mansi, purchasing their first home, and welcoming their twin boys, Aarav and Samar.

Practical Founders Podcast: Growth Equity for Efficient Scale-Up Founders

E-Commerce Checkout: The Future Is Autonomous

InsurTech Transforming the Role of Brokers and Agents

PeakSpan’s Thesis for ServiceUp: A $200B Industry Running on PDFs, Phone Calls, and Friction

Amazing Teams Podcast: You Can’t Clap with One Hand: Lessons from 55 Startups with Sanket Merchant

Navigating the Tariff Crossroads: Insights from PeakSpan’s Supply Chain Roundtable

A Match Made in Heaven: Why DIFM Automation & Agentic AI Are the Perfect Marriage

PeakSpan’s Thesis for Tapcheck: Series A Extension

PeakSpan PEC Roundtable: Insights from Top Sales Leaders on Sales Methodology, and More!

HVAC Field Service: Building The Jobsite of the Future

Why E-Commerce Will Kill Retail Sooner Than You Think

PeakSpan’s 2025 E-Commerce Logistics Outlook

B2B eCommerce Trends & Predictions for Future

We Pretty Damn Quickly Decided To Invest In PDQ: Here’s Why

Key findings from the PeakSpan Ibbaka Net Revenue Retention Research

The Back Office Infinity Stones Gauntlet — PeakSpan’s Thesis for Finally

Part IV: Spring 2024 eCommerce Technology Trends from a Buyer’s POV

PeakSpan’s Thesis for Abre

Part III: Spring 2024 eCommerce Technology Trends from a Buyer’s POV

Growth-Stage Venture Capital Strategies | Matt Melymuka | MSP #269

.png)